You're An NRI Watching India Compound From Dubai

You earn well. You save diligently. So why is your money sitting idle while India compounds?

At lunch, you glance out from your Dubai office. Construction workers toiling in the baking heat. Men and women from across the world, working hard to send money back home. Just like you.

Then you check your phone. Your cousin in Pune just bought a new home. The Sensex keeps hitting fresh highs. Every other headline seems to be about someone you know finding a way into the markets.

And after the money you send home and your living expenses, a quiet question surfaces. Is your money actually working as hard as you are? Or is it just sitting in a savings account earning 4%, when the markets could give you so much more?

That thought crosses the mind of a large number of NRIs in the Gulf, the US, the UK, and Europe. You’d love to put your money somewhere it can actually grow, somewhere that builds toward your retirement. But you don’t quite know how to go about it, or what it takes.

There’s a way. Let’s walk through it.

Why NRIs Choose Not To Invest In India

For many, it’s the dread of the paperwork. Arranging documents, updating Aadhaar, standing in lines, sorting out bank details. When you fly home, you want to see family, attend a wedding, celebrate something. Not spend three days fixing your KYC.

For others, the intent is there but the path isn’t clear. They’d happily invest in mutual funds or equities, but don’t know how to convert their existing accounts to reflect their NRI status. And the fear of getting scammed somewhere along the way is real.

These hurdles have become far easier to clear than they once were. But the old adage that “investing in India is complicated” lingers, and it quietly becomes a self-fulfilling reason to keep missing the opportunity.

The Four Routes Into India

For an NRI, investing in India doesn’t have to be rocket science. There are four clear routes.

Route 1: Smallcases

These are curated baskets of stocks, picked by professionals, that you buy through a broker and hold in your own demat account. You own the stocks directly, with full transparency.

You can start with around ₹10,000 plus a subscription fee. Ideal for someone who wants to begin without a large minimum and stay in control. The catch worth knowing: Smallcases are available to NRIs, but only through select brokers that support NRI demat accounts.

Route 2: Portfolio Management Services (PMS)

A professionally managed equity portfolio, built and run for you by a SEBI-registered manager. Aimed at NRIs who want to invest more than ₹50 lakh with a hands-off approach. A manager handles the strategy and helps you navigate the NRE/NRO setup as needed.

The ₹50 lakh minimum is set by SEBI. This is where most serious NRI capital goes, because it removes the operational burden entirely.

Route 3: Alternative Investment Funds (AIF)

These pooled investment vehicles offer more flexibility than mutual funds. Category III AIFs invest in listed equity with more sophisticated strategies. Aimed at HNI NRIs, with a minimum ticket size of ₹1 crore, for those who want differentiated strategies and exposure beyond standard products.

Route 4: The GIFT City / DIFC Route

The newest route, and the most relevant for Gulf NRIs. Investing into India through international financial centres, GIFT City in India being the key one, lets you access dollar-denominated, regulatory-clean exposure to India with attractive tax efficiencies. For NRIs in Dubai who want exposure without the full repatriation complexity, this is increasingly the gateway worth understanding.

The Three Questions Every NRI Asks

These are good opportunities. But before acting, every NRI wants clarity on three things.

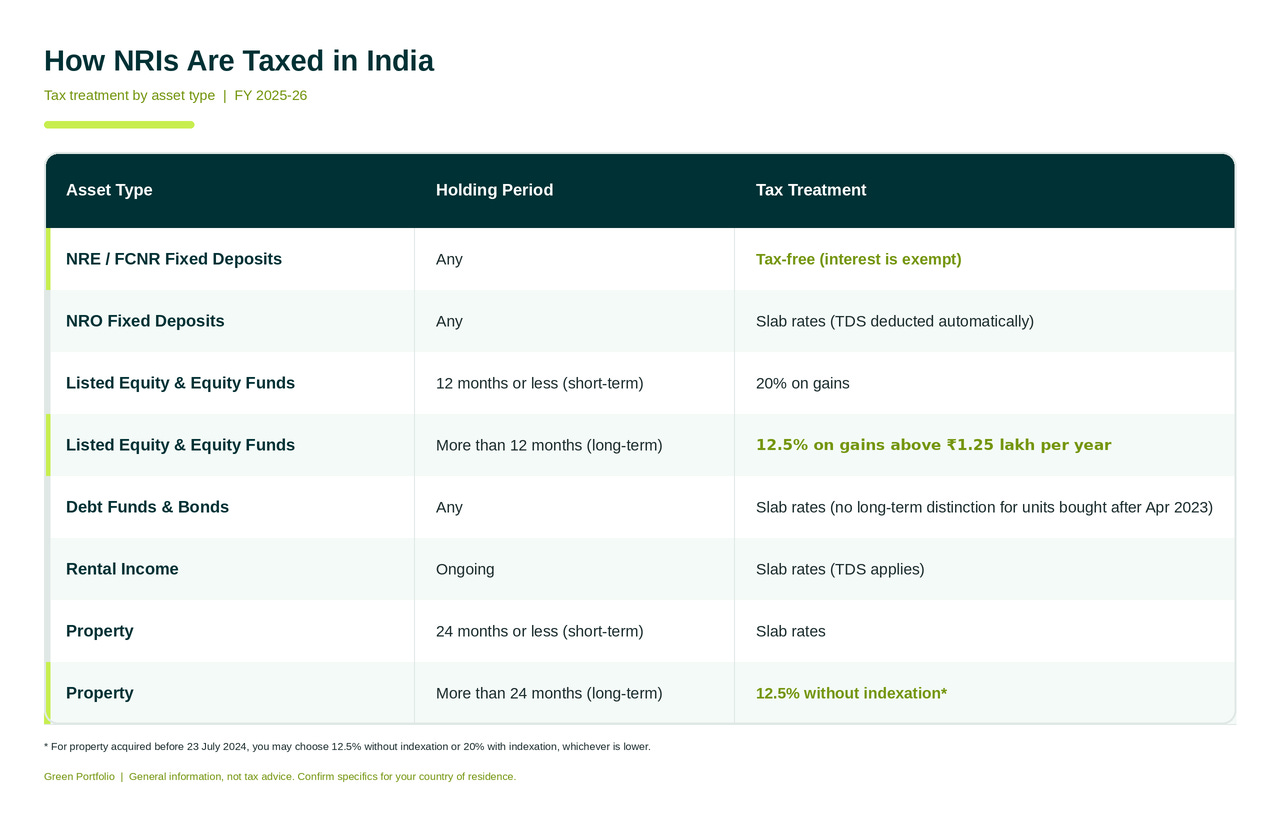

Question 1: How am I taxed?

Here’s the short version. You pay tax on India-sourced gains in India. But Double Taxation Avoidance Agreements (DTAA) between India and countries like the UAE, the US, the UK, and Singapore mean you are generally not taxed on the same income twice. For most NRIs, the fear of double taxation is unfounded.

Once your account status is established as NRE, NRO, or FCNR, the tax treatment becomes fairly transparent.

*For property acquired before 23 July 2024, you may choose between 12.5% without indexation or 20% with indexation, whichever is lower.

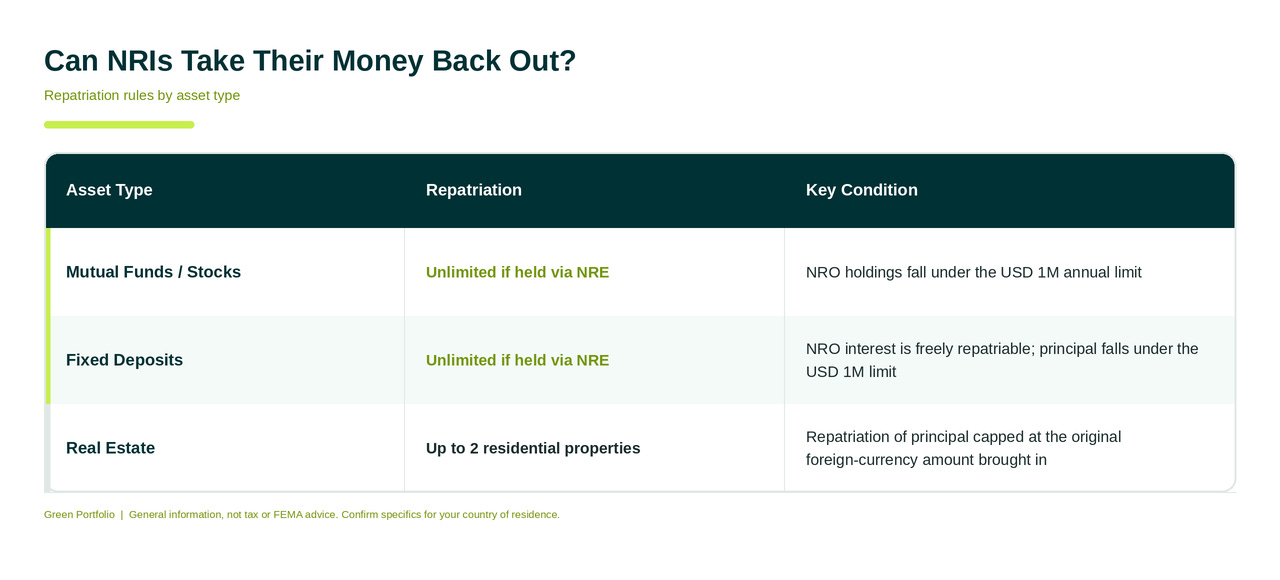

Question 2: Can I take my money back out?

Yes. It depends on the type of account you hold.

With a Non-Resident External (NRE) account, funds are freely repatriable. You can move money back out without an annual cap. With a Non-Resident Ordinary (NRO) account, repatriation is capped at USD 1 million per financial year, after applicable taxes are paid.

Question 3: Is the KYC and onboarding actually painful?

Far less than it used to be. If you have an Aadhaar linked to an Indian mobile number, most of your e-KYC can be completed digitally. Attesting foreign documents can be a hurdle, but it’s a one-time one, handled either by couriering documents to India or through video KYC.

It varies case to case, but in most situations, any friction here is a one-time issue that doesn’t resurface once it’s sorted.

The Mistake Most NRIs Make

Most NRIs who come home eventually get their paperwork in order. But many never get around to investing it in the right places.

It usually goes like this. Leftover money at the end of a long visit gets parked in a low-yield NRE fixed deposit, with a quiet promise to “move it somewhere better later.” Later rarely comes, because the whole idea of investing feels daunting.

What gets missed is the real cost of that delay. A fixed deposit at 6% barely keeps pace with inflation. Indian equity has historically compounded at meaningfully higher rates over the long run. Over a 10-year horizon, the gap between “safe and idle” and “invested and compounding” runs into serious money.

Safe and idle is still a decision. And it’s an expensive one.

A Clear Path In

This is exactly the gap we help NRIs close. As a SEBI-registered firm, Green Portfolio has helped NRIs across the Gulf, Singapore, the UK, and the US deploy their savings into Indian markets, with the onboarding, documentation, and tax complexity handled by our team.

Many start with Smallcases, then move into PMS and AIF as their capital grows. The path is simpler than the confusion around it suggests.

If you’ve been watching India compound from the outside and want a clear path in, that’s exactly the conversation we’re built for.

Closing Thoughts

The next time your cousin posts about his latest investment, you won’t feel that quiet pang of being left out.

India’s growth story was never closed to you. It was just never explained clearly. Now it has been.

You don’t have to watch from Dubai anymore. You can participate from there.

Disclaimer: This newsletter is for informational and educational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell any securities. Views expressed are based on publicly available information as of the date of publication and may change without notice. Please consult a qualified financial adviser before making any investment decision.

This is general information and not personalised tax or investment advice. Tax rates and repatriation rules are current to the date of publication and can vary by your country of residence. NRIs should confirm the specifics applicable to their situation with a qualified advisor before investing.