Your mutual fund is quietly charging you ₹2-3 lakhs over 15 years. Legally.

Even though you may have seen a profit on your MF statement, that doesn’t mean you’re getting a good deal. Increased charges may be eating into your returns in practice, and you may never have noticed

Rakesh, 32, a well heeled, successful IT professional, has been consistently investing in Mutual Funds through SIPs for almost 10 years now. It all started when a relationship manager sat him down and explained why SIPs were important, and how they can help him secure his future. Convinced, he signed up for 4 monthly SIPs covering all asset classes between them worth Rs.10,000. .

Since then, he has seen his corpus grow over the years, compounding by about 12% CAGR on average, based on the average market returns in the last 15 years. He has been content with the returns he’s earned so far on his corpus of Rs. 18,00,000 for the ten years he’s been investing, even as the market witnessed its share of ups and downs.

How Mutual Funds are expected to work

For investors like Rakesh, the portfolio’s performance has mostly meant two things.

A. How much have I invested? and

B. How much have I made from these investments?

There are countless investors like Rakesh out there, who have booked good profits from their SIPs and continue to lay their trust in them. By continuing to trust his RM and the Mutual Funds Sahi Hai campaign, Rakesh continued with his SIPs, never bothering to question them. Only if he had known what to expect, and how much to expect, he could’ve got a better deal. His investments had the potential to grow faster and better, but the benefit of doubt still persists. And he will still not know that he could’ve earned more, if only someone had told him.

Why Mutual Funds fail at meeting expectations

For investors like Rakesh, Mutual Funds have always been the easiest way to invest in the capital markets, with advisors being the point of guidance in case of any queries. But not all investment advisors align their clients needs with their own, and many investors do not bother to ask the right questions.

In Rakesh’s case, this has meant a difference of about Rs.2-3 lakh. The reason? His advisor suggested a MF scheme that offered him the best commissions, and Rakesh readily complied.

The commission structure inherent bias: Up till then (and maybe even now) Rakesh didn’t know why he could have earned more. The secret lies in the two types of MF plans offered- Regular and Direct

What a Regular plan is: When you buy a mutual fund through a distributor, in this case, through a financial advisor or a Relationship Manager, you are buying a Regular plan. The AMC pays the distributor a commission, called trail commission, every year. This commission comes from your fund’s expense ratio.

What a Direct plan is: When you buy directly from the AMC or a SEBI-registered investment advisor, there is no distributor. No commission. The expense ratio is lower. The full return stays with you.

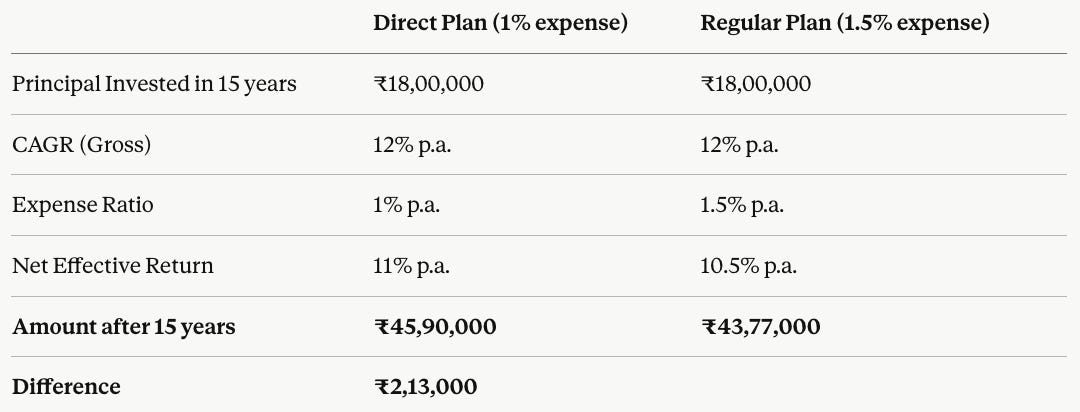

To make things easier to understand, here’s the maths. On a 15 year SIP with a corpus of Rs.18 lakh, this is the difference in returns considering an average CAGR of 12% the markets have given.

Now, this picture will get worse if you increase SIP amount, time or returns. If Rakesh knew about regular plans, he could’ve earned almost 11.8% more returns than he did- almost worth Rs. 2.13 lakhs. The 0.5% difference in expense ratio made all the difference here, and could’ve made a better difference if he had switched to a regular plan anytime earlier.

This is the challenge that millions of investors like Rakesh face everyday- the lack of proper guidance. Blame misselling or conflict of interest.

The inherent bias

With 50 Mutual Fund houses managing more than 1500 funds competing for your attention, the conflict of interest problem continues to plague the market. This is like the doctor who suggests medicines that get him the best commissions, even if cheaper alternatives are available. In this case, three things happen when your advisor is paid by commissions:

1. What they sell you may not be in your interest. The commission structure may dictate which funds they suggest to you, especially for regular plans. Sometimes, they may have a target to meet, and your SIP could be the last hurdle in meeting that.

2. They may not understand your risk appetite or choose to ignore it. Someone who is 28-year-old with a stable income and a 20-year horizon should be predominantly equity. But if a conservative debt fund pays a better commission this month, the nudge may go the other way. This is not always deliberate. Sometimes the advisor themselves is not trained to have this conversation. Either way, you bear the consequence.

3. They have no incentive to tell you when to exit. According to the latest SPIVA (S&P Indices Versus Active) India report for 2025, about 76% of large cap Mutual Funds have underperformed the S&P India Large and Midcap Index. Many of the funds have been merged with other funds or liquidated, and they no longer exist now.

A well intentioned advisor would review your portfolio periodically, and suggest you to switch funds if they have been underforming lately. Axis Large Cap Fund and Aditya Birla Sun Life Frontline Equity, once considered titans in the industry, are now at the bottom of the indices, as they have struggled to beat the returns. Yet many continue to invest in them by SIP, as their advisors continue to benefit from the status quo.

Though Mutual Funds now have star ratings for their risks- like those you get on your electronics to judge their energy efficiency- but most don’t know that these are based on data from the past 3 years, not the next 3.

Investor Checklist: Is this you?

Before you read further, answer these four questions

Do you know if your funds are Regular or Direct plans?

Can you name what each of your SIPs is meant to fund?

Has your advisor ever told you to exit a fund?

Do you know what your total expense ratio is across your portfolio?

If you answered no to more than two, this is for you.

The Solution

The SPIVA India report further states that most actively managed funds haven’t beat the index, yet investors continue to pay for them. Besides that, many funds hold the same stocks, affecting the efficiency of your investments. To address these, we built the Roadmap Series helping investors like Rakesh to have the right long term expectations. It recommends:

Direct plans only. No distributor between you and your fund. No trail commission leaving your corpus. The full return is yours.

Flat subscription model: Most investors don’t realise this, but the fact is that traditional advisors earn more as your portfolio grows. With a flat subscription model, the charges remain the same, whether you invest Rs. 1 lakh or Rs. 50 lakh- the only incentive is your outcome, not your corpus size.

Goal-based baskets. Not a random collection of funds. Structured around milestones, so every rupee has a destination.

The unknown missed opportunity

For investors like Rakesh, asking the wrong questions has meant losing out on lakhs in missed returns. This could have been averted if he had the right guidance that has been missing for millions of investors across the country, most of whom continue to hold SIPs without understanding how they should work and could work.

Rakesh now knows what he missed. The question is whether you’ll find out the same way he did or before.