The rupee crashed. Some Indians just got richer.

Rupee crashes 82 paise to close at all-time low of 95.31 against U.S. dollar.

Rupee at 95.6: Currency crashes to record low as US-Iran ceasefire jitters send oil soaring.

Over the past four months, headlines like these have caused waves of concern, while the world worries about the economic fallout from the US-Iran war.

For India, this has meant the rupee depreciating 6% on a year-to-date basis, with fears that it could soon cross the ₹100 mark, breaching an imaginary Lakshman Rekha that has spooked people for weeks.

But should it?

Arvind Panagariya, the Finance Commission Chairman, doesn't think so. In a series of posts, he argued that any attempt to artificially arrest the fall of the rupee would be nothing more than a band-aid for the country. The rupee, in his view, should be allowed to adjust naturally, because it can recover on its own as the geopolitical and economic situation shifts. Any intervention right now, whether through dollar-rupee swaps, repo rate changes, or dollar bond issues, will make little real difference. The falling rupee is a consequence of the global moment, not an indicator of something broken at home.

Here is the point most people are missing.

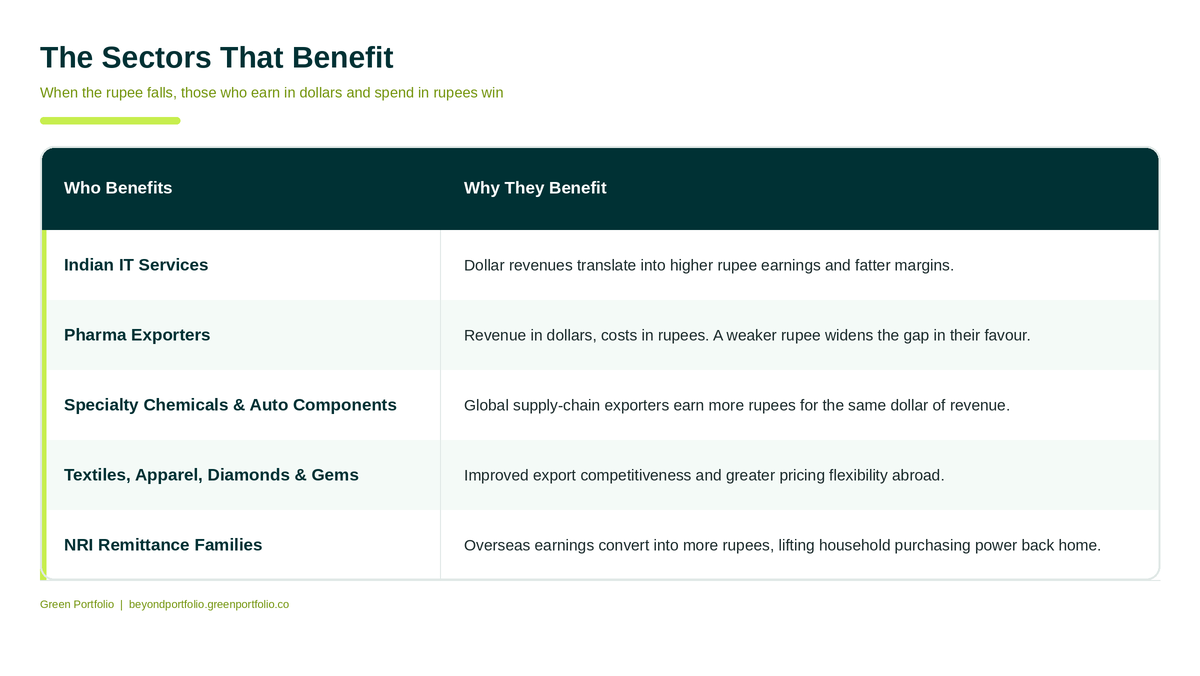

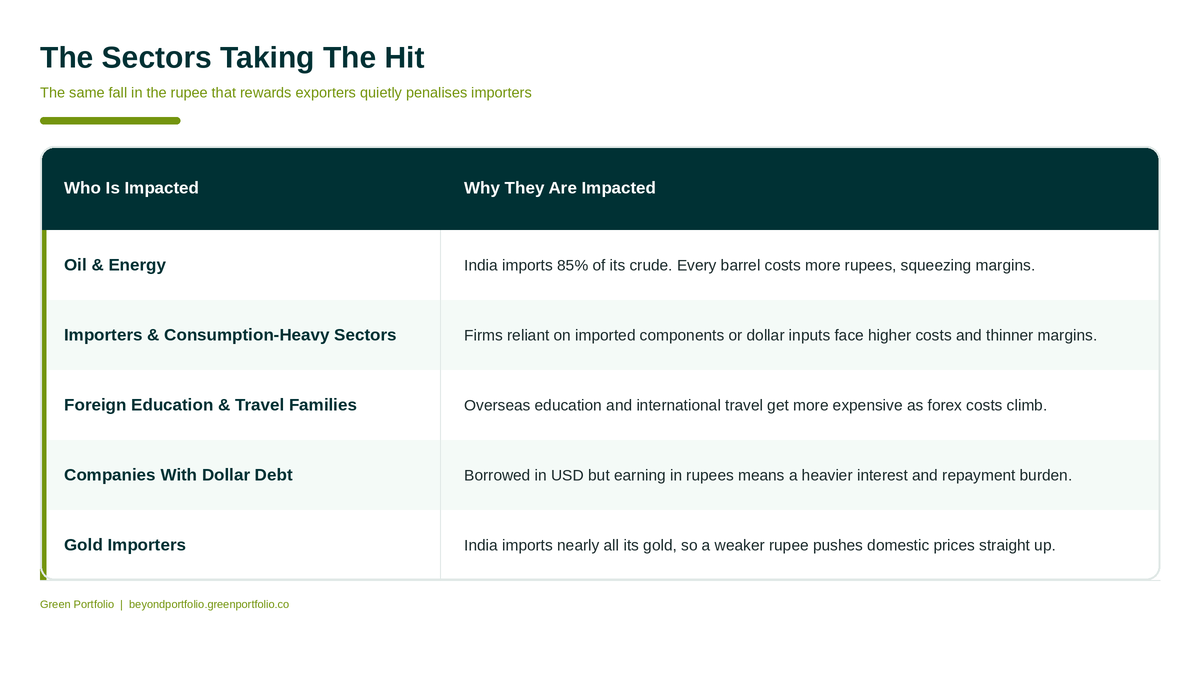

A falling rupee is not a national loss. It is a transfer of wealth between sectors. Importers lose. Exporters win. Oil burns. IT margins expand. The same news that is making some Indians poorer is quietly making others richer. The only question that matters is which side your portfolio sits on.

In this newsletter, we’ll look at how similar moments have played out before, and why you shouldn’t let the panic get to you.

What actually happened?

The US-Israel war with Iran has been the primary trigger. The blockade of the Strait of Hormuz sent oil soaring to $115 a barrel, which meant more foreign exchange leaving the country to pay for imports. Add to that sustained FII outflows of over $19 billion net so far this year, with $11 billion pulled in March alone, the sharpest monthly outflow since October 2024.

That part has dominated the headlines. You feel it every time you fill your tank. But there is a flipside to all of this, and it just depends on how and when you’re willing to see it.

So let’s start there. Every currency move has winners and losers. Here are both.

The Sectors That Benefit

The Sectors taking the hit

It hurts the economy. It also helps it. The same news, two outcomes. Some balance sheets get stronger, others get weaker, and most retail investors have no idea which side of that line their own portfolio sits on.

But the markets have been here before. These moments have spooked investors in the past, and every time, the panic turned out to be temporary.

The Historical Pattern

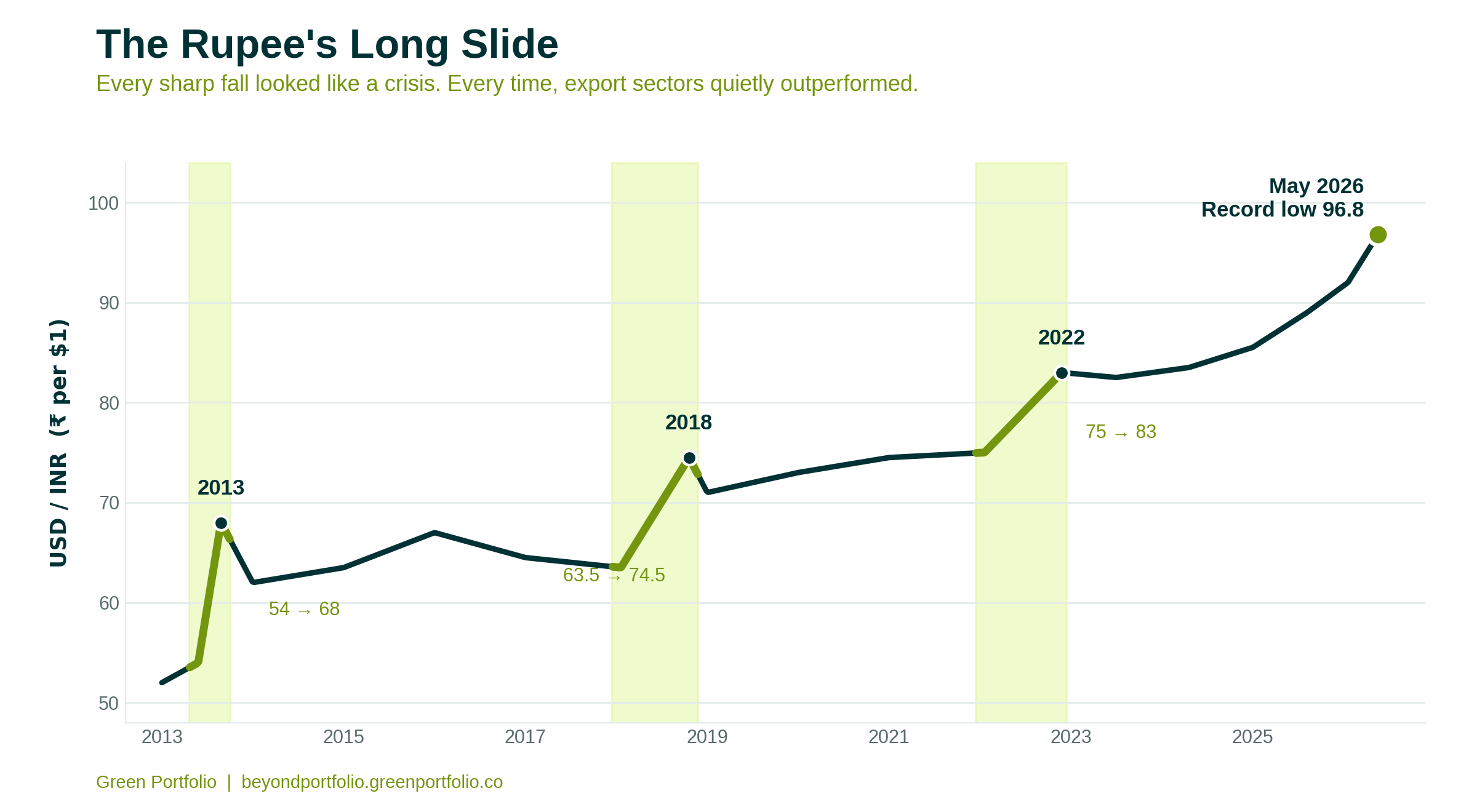

Three episodes of prolonged rupee depreciation over the past fifteen years tell a remarkably consistent story.

2013, the taper tantrum. The rupee fell sharply, from 54 in May to 68 in August, as markets reacted to the US Federal Reserve winding down its bond-buying program. India was running a 4.8% current account deficit, driven by heavy crude and gold imports, spending more forex than it was earning. It looked grim at the time. Yet patient investors saw the Nifty outperform by over 25% in the following 18 months.

2018, the emerging market crisis. The rupee slid from 63.50 in January to 74.50 in October, as surging crude prices and US tax cuts triggered FII outflows across emerging markets. As the rupee weakened, export-oriented pharma and IT firms outperformed the broader market comfortably.

2022, the Fed hike cycle. The rupee fell from 75 to 83 as the Russia-Ukraine war sent commodity prices soaring. That roughly 10% depreciation boosted IT margins, helping TCS, Infosys, and HCL outperform. Pharma exporters rode the same tailwind.

Three episodes. Fifteen years. The same playbook each time, and the same sectors quietly rewarded while everyone else watched the headlines and worried.

The Behavioural Mistake Most Indians Are About To Make

When the news shows the rupee falling, Indian investors tend to do one of two things. Both are wrong.

The first is rushing into dollar assets to “hedge the rupee.” But here’s the thing. You don’t import goods. You don’t export them. You don’t save for your retirement in dollars. The currency mismatch that worries the government is not your problem to solve, and trying to solve it usually creates a new one.

The second is panic-selling Indian equities. The headline fuels that instinct that things must be bad if the rupee is falling. So investors end up panic-selling their export-heavy holdings, the very ones most likely to deliver meaningful returns over the long run.

The better response is simpler. Look at your portfolio. Ask which sectors benefit and which suffer. Then act accordingly.

What To Actually Do

If you’re worried about a weaker rupee affecting your portfolio, three concrete steps.

First, audit your portfolio for currency exposure. Not just what sectors you own, but what currency your underlying companies actually earn in. If you’re heavy on banks, FMCG, and consumption, you own rupee-cost, rupee-revenue companies. They feel the pain of inflation without the offset of a dollar tailwind.

Second, don’t chase the IT or pharma rally blindly. A weak rupee opens a window for these sectors, but export exposure and underlying growth matter just as much. The currency is one input, not the entire thesis.

Third, resist the urge to chase dollar assets directly. Your home, your retirement, your family’s expenses are all in rupees. Buying US stocks or dollar funds to hedge introduces a currency mismatch you don’t actually need. The cleaner play on rupee weakness is owning Indian companies that earn in dollars, not parking money in dollar assets abroad.

That last point is exactly the kind of positioning we build into our portfolios at GreenPortfolio. If you’d like to see how this thesis translates into actual stock selection, our expert-curated portfolio is designed for precisely this kind of scenario. Explore our smallcase.

Closing Thoughts

The next time someone forwards you the worried screenshot of the rupee chart, remember this.

A weaker rupee doesn’t make India poorer. It makes some Indians poorer and other Indians richer.

The question worth asking isn’t “is the rupee falling?”

The question is “which side of the rupee is my portfolio on?”

Disclaimer: This newsletter is for informational and educational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell any securities. Views expressed are based on publicly available information as of the date of publication and may change without notice. Please consult a qualified financial adviser before making any investment decision.