The mutual fund you picked does not matter

The 6 Rules that matter more. Most underperformance is not a fund problem. It is a behaviour problem hiding inside a fund problem.

Every year, millions of Indian investors spend hours researching mutual funds.

Star ratings. Expense ratios. Alpha. Sharpe ratios. Rolling returns. Fund manager track records. Category rankings. They go deep, they compare carefully, and they make what feels like an informed decision.

And then they undo most of that work with six behavioural mistakes that no fund selection process can protect against.

The uncomfortable truth is this: for most retail investors, the gap between what their funds returned and what they actually earned is not a fund quality problem. It is a behaviour problem. The fund did its job. The investor did not let it.

Why Fund Selection Is the Wrong Starting Point

Fund selection matters. It is not irrelevant. But it is the fourth or fifth most important variable in long-term wealth creation, not the first.

The most important variables are upstream of fund selection entirely. How long you stay invested. Whether you pause during corrections. Whether you have a target that keeps you from switching. Whether your portfolio has a structure or just a collection of individual bets.

Get those wrong, and the best fund in the category will not save you. Get those right, and a decent fund in the right structure will compound reliably over time.

At Green Portfolio, we call the system that governs these variables the 6-Rule Discipline Protocol. It is not a checklist for picking funds. It is a framework for not undermining the funds you have already picked.

Here is what it covers.

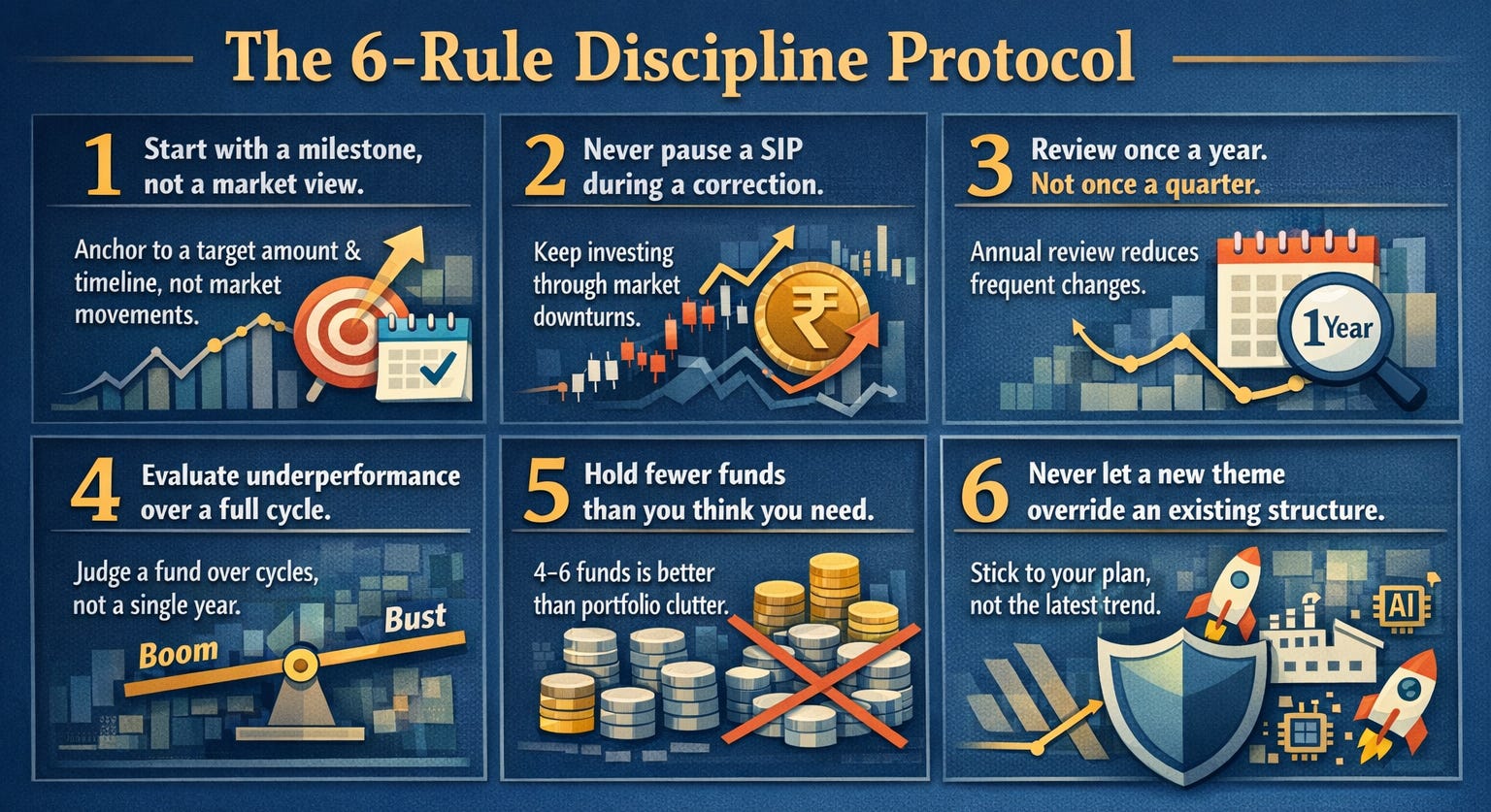

The 6-Rule Discipline Protocol

Rule 1: Start with a milestone, not a market view.

Every investment decision should be anchored to a target amount and a timeline, not to what the market is doing today. The milestone determines fund selection, SIP size, and review frequency. Without it, every market movement becomes a decision trigger it should not be.

Rule 2: Never pause a SIP during a correction.

A falling market is not a reason to stop investing. It is the mathematical best time to continue. The rupee cost averaging benefit of a SIP is most powerful precisely when markets feel worst. Pausing destroys compounding leverage at the moment it is most valuable.

Rule 3: Review once a year. Not once a quarter.

Frequent portfolio reviews produce frequent changes. Frequent changes produce tax drag, exit load costs, and the consistent human tendency to exit at lows and re-enter at highs. An annual review with a structured process is not laziness. It is the discipline to let compounding do its job.

Rule 4: Evaluate underperformance over a full cycle, not a calendar year.

A fund that underperforms for 12 months is not a broken fund. It may be a fund whose style is out of cycle. The decision to exit should be based on process integrity, not recent returns. Most switches made on 12-month underperformance are made at exactly the wrong time.

Rule 5: Hold fewer funds than you think you need.

Four to six funds across genuinely different categories covers most investors at most stages. Beyond that, you are adding overlap, not diversification. Complexity is not sophistication. It is a liability that compounds quietly over years.

Rule 6: Never let a new theme override an existing structure.

Defence is hot. Manufacturing is the next decade. AI-linked funds are gaining traction. Every year produces a new narrative that feels like a compelling reason to add a fund. The question is never whether the theme is real. The question is whether it belongs in your portfolio given your milestone, your timeline, and your existing structure. If the answer requires more than two sentences, the answer is probably no.

The Number

SEBI data consistently shows that the average Indian mutual fund investor significantly underperforms the funds they are invested in. The gap is not explained by fund quality. It is explained by entry and exit behaviour, most of which violates at least two of the six rules above.

The fund is not the problem. The investor is working against the fund.

What to Watch in Your Own Portfolio

Run your own portfolio against the six rules. For each rule, ask a simple yes or no.

Do you have a milestone anchoring your current portfolio? Have you paused any SIP in the last two years? Did your last portfolio review produce more than two fund changes? Have you exited a fund within 18 months of starting it? Do you currently hold more than six funds? Have you added a thematic or sectoral fund in the last year based on a market narrative?

If more than two answers make you uncomfortable, the portfolio has a behaviour problem, not a fund problem.

One Thing to Do This Week

Pick the one rule from the six that you have most consistently violated. Write it down. Treat it as the single constraint to fix before your next review. One rule corrected and held is worth more than six rules understood and ignored.

A Note Before You Go

The 6-Rule Discipline Protocol is not a theoretical framework. It is the behavioural backbone that The Wealth Roadmap is built around.

The milestone-based structure keeps Rule 1 intact by design. The rules-based rebalancing process handles Rules 3 and 4 so you do not have to rely on willpower. The curated basket of four to six funds per milestone handles Rule 5 from the start. The process-triggered review cadence handles Rule 6 every time a new theme starts trending.

The point is not to make discipline harder to maintain. It is to build a structure where discipline is the default, not the effort.

Green Portfolio is opening The Wealth Roadmap to the first 100 subscribers at 99% off the full subscription price.

Full access. The same research, the same process, the same fund selection framework behind Rs 1,000 Crore in AUM and 65,000 investors.

When 100 are gone, this price closes. No waitlist. No exceptions. No second round at this price, ever.

If the six rules above made you realise your portfolio has a behaviour problem worth fixing, this is where you fix it:The Wealth Roadmap

More coming soon.

Disclaimer: Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing. This newsletter is for educational and informational purposes only and does not constitute investment advice.