Anthropic is worth more than Switzerland.

The case against the most expensive technology IPO in history.

A company with one profitable quarter is about to list at the most expensive valuation in modern market history. The question worth asking isn’t whether AI is real. It’s whether the price being paid for it is.

A recent development has investors more excited than any IPO in modern memory.

A company is expected to go public by October 2026. It raised $65 billion in May. It is currently valued at $965 billion. Its annualised revenue has crossed $47 billion. By the time it lists, it will almost certainly cross the $1 trillion mark.

That number is larger than the GDP of Switzerland. Larger than Saudi Arabia. Roughly double the combined market capitalisation of every listed Indian bank put together.

We’re talking about Anthropic, the company behind Claude, the AI model that engineers, lawyers, and product managers across the world are quietly using to do their jobs faster than most leadership teams realise.

Behind the excitement is a fact almost no one is talking about.

Anthropic reported its first profitable quarter in June 2026.

Its first. In six years of operation. Three months ago.

The IPO is in October.

Two Companies. $1.8 Trillion. Almost No Profits.

On June 1, 2026, Anthropic filed confidentially for an IPO at a $965 billion valuation. OpenAI, the company that started the modern AI race, is expected to follow with its own listing by 2027.

Together, the two companies are projected to enter public markets at a combined valuation north of $1.8 trillion.

This is the most expensive technology IPO sequence in history. Revenues at both companies are growing at over 200% year on year. Enterprise adoption is accelerating. The story is real.

But neither company is cash flow positive. Neither has been for the entirety of its existence. And both are about to be valued like they have been.

For market insiders, that is the problem. There is enormous hope of future returns. There is no clarity on when those returns will arrive or whether they will arrive at all.

Welcome To A Market Without P/E Ratios

When you buy a stock, you are buying a future stream of profits. Every other metric, be it revenue multiples, user counts, growth rates, is a shortcut to estimate those profits when you cannot see them directly.

For most of public market history, that estimate has been expressed through the P/E ratio: how much you pay today for each rupee of profit you receive tomorrow. A reasonable P/E for a high-growth company sits between 30 and 40. The S&P 500 averages around 22.

You cannot calculate a P/E ratio for Anthropic. There is no E.

So the conversation has shifted. Investors now value AI companies on revenue multiples. Anthropic, at $965 billion in valuation and roughly $47 billion in annualised revenue, trades at about 20 times sales.

For context, Microsoft trades at 13 times revenue. Apple at 8. Google at 6. Salesforce and ServiceNow, the enterprise software giants whose business Claude might one day disrupt, trade at 10 to 15 times revenue today and they earned those multiples over two decades of consistent profitability.

Anthropic is being valued as if it has already done the same. Five years into its existence. With one profitable quarter behind it.

Every time markets have stopped using P/E ratios as a valuation framework, history has called that a warning sign.

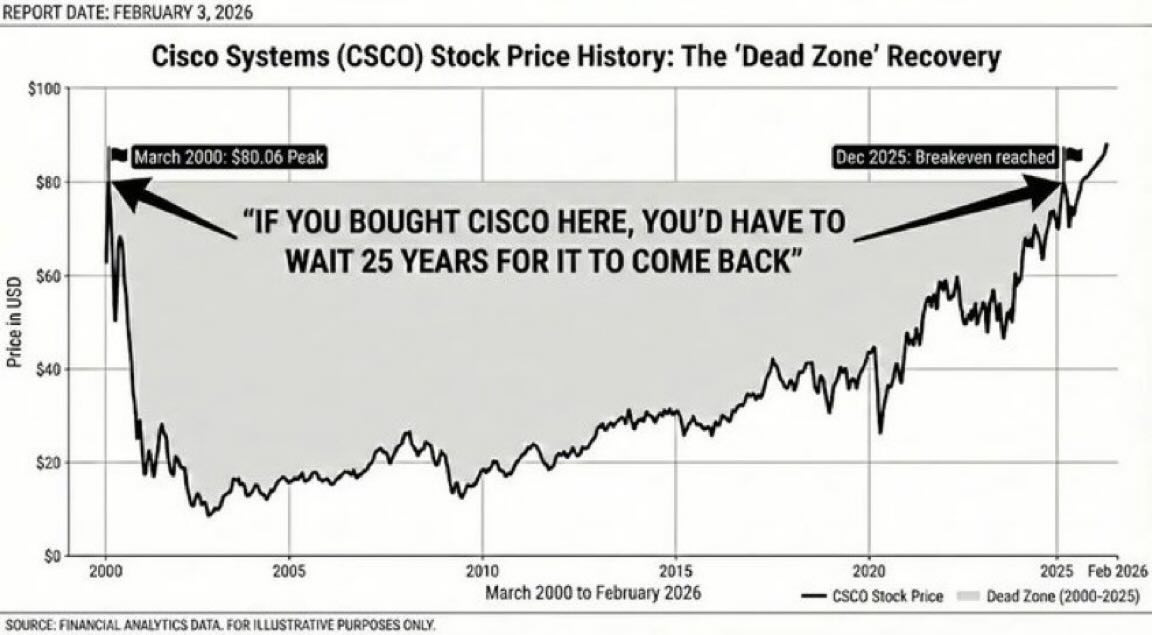

Cisco Was Right About The Internet. It Still Took 24 Years To Recover.

In March 2000, Cisco Systems was the most valuable company on earth.

Its routers were the plumbing of the internet. The narrative was unimpeachable. Every business in the world would need Cisco hardware to participate in the future. The stock peaked at $80. The valuation hit $555 billion.

Within 30 months, the stock was at $8.

Here is the part most retellings of the dot-com bubble leave out.

Cisco’s revenues kept growing. Its profits kept growing. The company became, and remains, one of the most important infrastructure businesses in the world. The narrative was completely right.

It took 24 years for the stock to reclaim $80.

The technology won. The investors who bought it at the top didn’t. Anyone who held Cisco from March 2000 had to wait until 2024 to break even, ignoring inflation, while paying the opportunity cost of holding capital in an asset that did nothing for two decades.

Being right about the future is not the same as being right about the price.

The Six Words That Have Ended Every Bubble In History

The honest comparison between today and the year 2000 has to acknowledge what is genuinely different.

AI companies today have real revenue, not just user counts. Enterprise adoption is faster than dot-com era consumer adoption. Productivity gains from AI are measurable in ways the internet wasn’t immediately. The underlying technology is more developed at this stage of the cycle than the internet was in 1999.

What is structurally identical is the part that should make a careful investor pause. Investors are paying for a future that has not been earned. Valuations rely on growth rates continuing for years without interruption. Pricing assumes no major competitor, no regulatory shock, no technology shift. And retail investors are being told, repeatedly and confidently, that they cannot afford to miss this.

That last similarity is the one history teaches us to fear.

Every speculative bubble of the last fifty years has ended on the same six words: you can’t afford to miss this. The Japanese real estate bubble of the 1980s. The dot-com bubble of 2000. The US housing bubble of 2007. The crypto bubble of 2021.

When markets tell you that the cost of waiting is greater than the cost of being wrong, that is precisely the moment that history says you can afford to wait.

So What Should Indian Investors Actually Do?

Here is the part where this stops being a story about Silicon Valley.

When Anthropic and OpenAI list, the temptation for Indian investors will be enormous. US brokerage apps will make participation one tap. Fractional share platforms will advertise it everywhere. International mutual funds will quietly add exposure to capture the narrative.

Most retail investors will buy in the first six months after listing. That is, statistically, the worst time to own a hyped IPO. The post-IPO drift downward in the first twelve months is one of the most consistent patterns in modern market history. Hype peaks at listing. Earnings disappoint at some point in year one. Long-term holders enter at lower prices than first-day buyers, almost without exception.

But there is a more important point.

The most interesting AI exposure for an Indian investor isn’t in California. It’s in India.

India is building the infrastructure layer of the global AI buildout. Data centres. Power generation. Electronics manufacturing. Fibre networks. These companies are growing alongside Anthropic and OpenAI. They benefit from every dollar of AI capital expenditure globally, regardless of which model wins the race.

They trade at 30 to 40 times earnings. Not 20 times revenue with no profit.

They have actual earnings. They have valuations that traditional frameworks can still measure. And they are not betting on which model wins the AI race. They are selling shovels to everyone in the race.

This is exactly the thesis behind our Bharat Tech Infra Tracker. A curated portfolio of Indian companies building the infrastructure layer of the AI buildout. The companies that benefit when AI scales, without the speculation of pricing a $1 trillion valuation on a company that turned profitable three months ago.

Same theme. Sane prices.

[Explore Bharat Tech Infra Tracker]

The Quiet Question Worth Asking

A $965 billion valuation. A company with one profitable quarter. An IPO race the entire technology world is watching.

AI is real. The companies are real. The opportunity is real.

Cisco was real too. The people who bought Cisco at $80 are still waiting to be made whole, even after the company proved every part of its original narrative correct.

The technology won.

They didn’t.

Be excited about AI.

Be careful about the price.

Disclaimer: This newsletter is for informational and educational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell any securities. Views expressed are based on publicly available information as of the date of publication and may change without notice. Please consult a qualified financial adviser before making any investment decision.