AI Shock, IT Selloff: Is India’s IT Premium Breaking?

Indian IT built its edge on cost-effective talent and strong digital execution for global clients. Now, surging AI demand is forcing rapid integration into core services.

India’s IT sector has been the ‘crown jewel’ of the economy for more than 25 years, with incremental growth reaching an almost 25% share in India’s overall export revenues in the last decade.

So far, this has depended on a recurring, predictable model: a large pool of English-speaking, skilled engineers delivering IT solutions cheaper and faster than their Western counterparts. Over the years, this model became India’s leading export earner, growing at almost 20% every year, eventually accounting for almost 49% of India’s services exports.

All of this depended on incremental skill development amongst the IT firms, with new technologies regularly replacing the old methods.

But that reputation has increasingly come under threat, by a technology that has become both a threat and an opportunity for the IT sector: AI. For leading IT companies, the old model will not work the way it used to, forcing them to adapt to meet client expectations, even bending over backwards to do so.

What India got right (until now)

India’s young population, along with its eagerness to upskill, has been at the core of this value creation. With every successive technological advancement, there have been scores of youngsters getting trained in these technologies to align these needs to client demands. This army of skilled youngsters helped the likes of TCS, Infosys and Wipro cement their status as digital ‘enablers’ allowing multinationals to keep themselves with, if not ahead, of the curve.

But that status is highly dependent on the ever evolving market conditions. And it NEVER works in the way you’d expect.

The unpredictable, discretionary threat

In 2023, American Insurer Transamerica terminated its $2 billion IT services contract with TCS two years ahead of schedule, citing ‘challenging macro economics’. The deal, once regarded as the biggest ever when signed in 2018, was meant to consolidate Transamerica’s more than 10 million policies on a single platform.

As part of the deal, TCS had hired almost 2,200 Transamerica employees, while onboarding another 2,000-odd employees on the project. When the contract ended, these employees had to be transitioned to other projects within TCS.

Though analysts claimed that this development was a ‘sentimental’ setback that didn’t affect its valuations, it showed how vulnerable the IT industry has been to external, arbitrary decisions. Of late, large players like TCS, Infosys and Wipro are regularly in the news, with reports of multi year, multi million dollar deals with clients signed. Every quarter, the companies’ success is measured by the number (and value) of these mega deals signed as the primary barometer of growth.

Though these help in boosting optics, it is anything. The harsh truth? IT revenues remain at the mercy of the clients’ discretion, with these mega contracts carrying hidden pricing concessions, forcing them to sacrifice margins if need be.

The elephant in the room: AI

With AI led tools promising to downsize teams and costs, clients are now forcing the IT companies to realign their traditional productivity barometers:

Outcome based pricing

Clients now demand an engagement model that measures outcome and solutions rather than hours worked or team strength. The rationale of payments rests on the ‘effectiveness’ of the digital transformation solutions, where the modules actually help in reducing costs and time rather than merely completing the project. For the IT companies, this has reduced the importance of manpower, as project managers are pressed to use AI-enabled solutions to meet outcomes, effectively increasing the risk associated with the project deliverables without making predictable upfront investments.

Competition

Clients are now actively vetting proposals to see how the solutions actually help them stay ahead of their competition through their digital solutions, rather than just merely boosting digital adoption of their operations. The proposals who use AI in the most efficient way usually wins here.

Clients are now vetting proposals to understand how the team uses product led AI vendors and platform-based automations(for example, using Infosys Topaz or TCS AI.Cloud) to boost delivery timelines,rather than just merely boosting digital automation for the company’s operations. They also judge how the companies use internal teams, hyperscalers and various AI-led vendors to meet delivery outcomes, making it increasingly challenging for the IT companies to win contracts.

The impact on the IT companies operations

This shift in the market dynamics has directly impacted IT companies revenues, which grew robustly in the 2010s following its pre-AI model famous for their mass hiring sprees following large order wins.

According to NASSCOM, India’s IT industry’s revenues grew just 5.1% in 2025, a far cry from the double digit booms witnessed after the pandemic and before AI got mainstreamed.

The companies’ operating profit margins (OPMs) have faced significant pressures, narrowing almost 70-100 bps due to higher wages for specialised talent and competitive pricing pressures to win large deals.

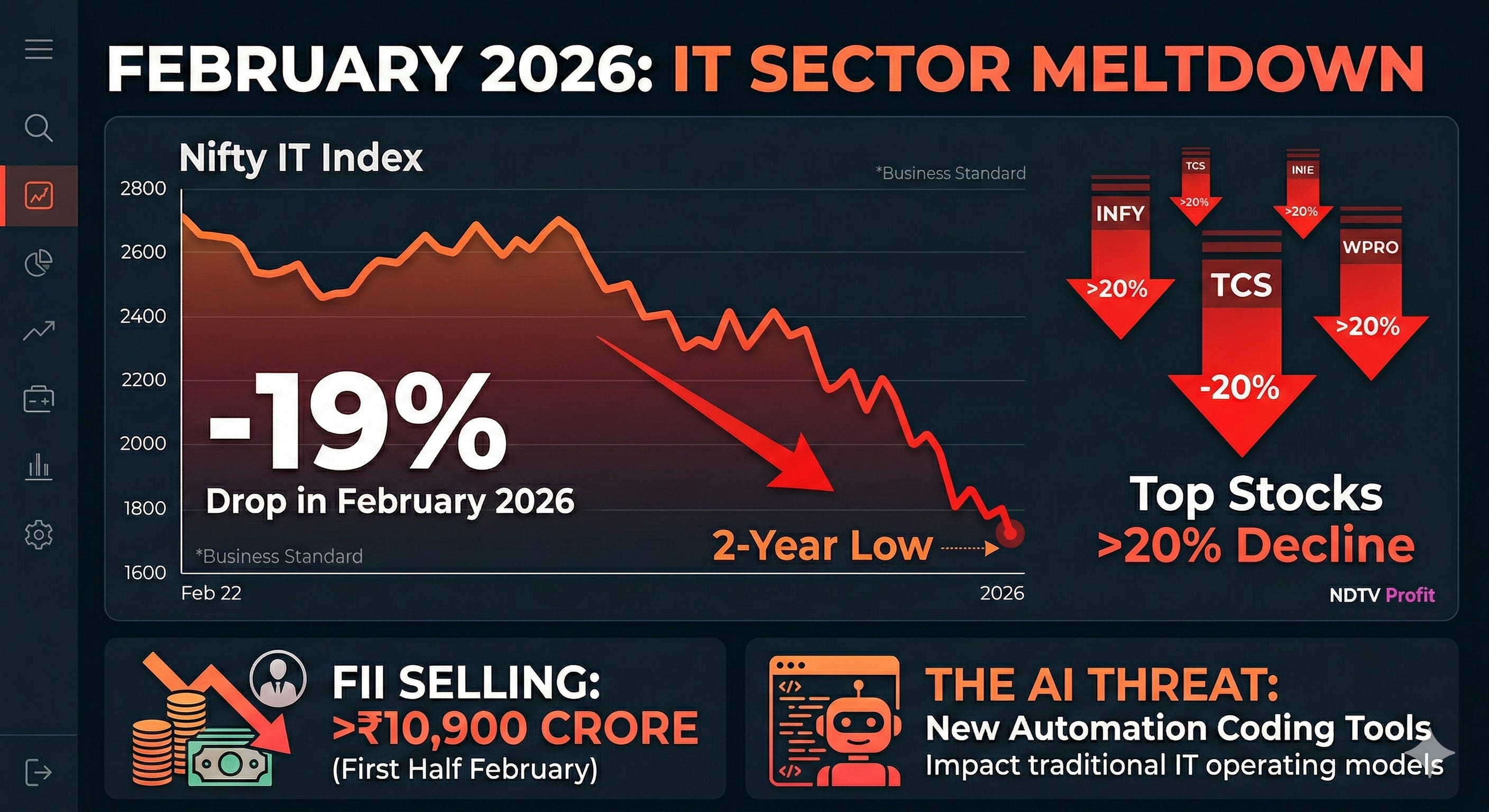

The February 2026 IT meltdown

After years of consistent capital appreciation, the markets are now starting to worry about the IT sector, especially as the Nifty IT Index has plummeted almost 19% in February 2026, reaching a 2 year low, according to a report by Businesss Standard

According to the report, several leading IT stocks have fallen more than 20%, with FIIs selling more than ₹10,900 crore of IT stocks in the first half of February alone, according to a report by NDTV Profit. This comes after new AI automation coding tools launched by the likes of Anthropic (specifically Claude Cowork Agent and Claude Code) have been in the news, threatening the IT companies traditional operating models.

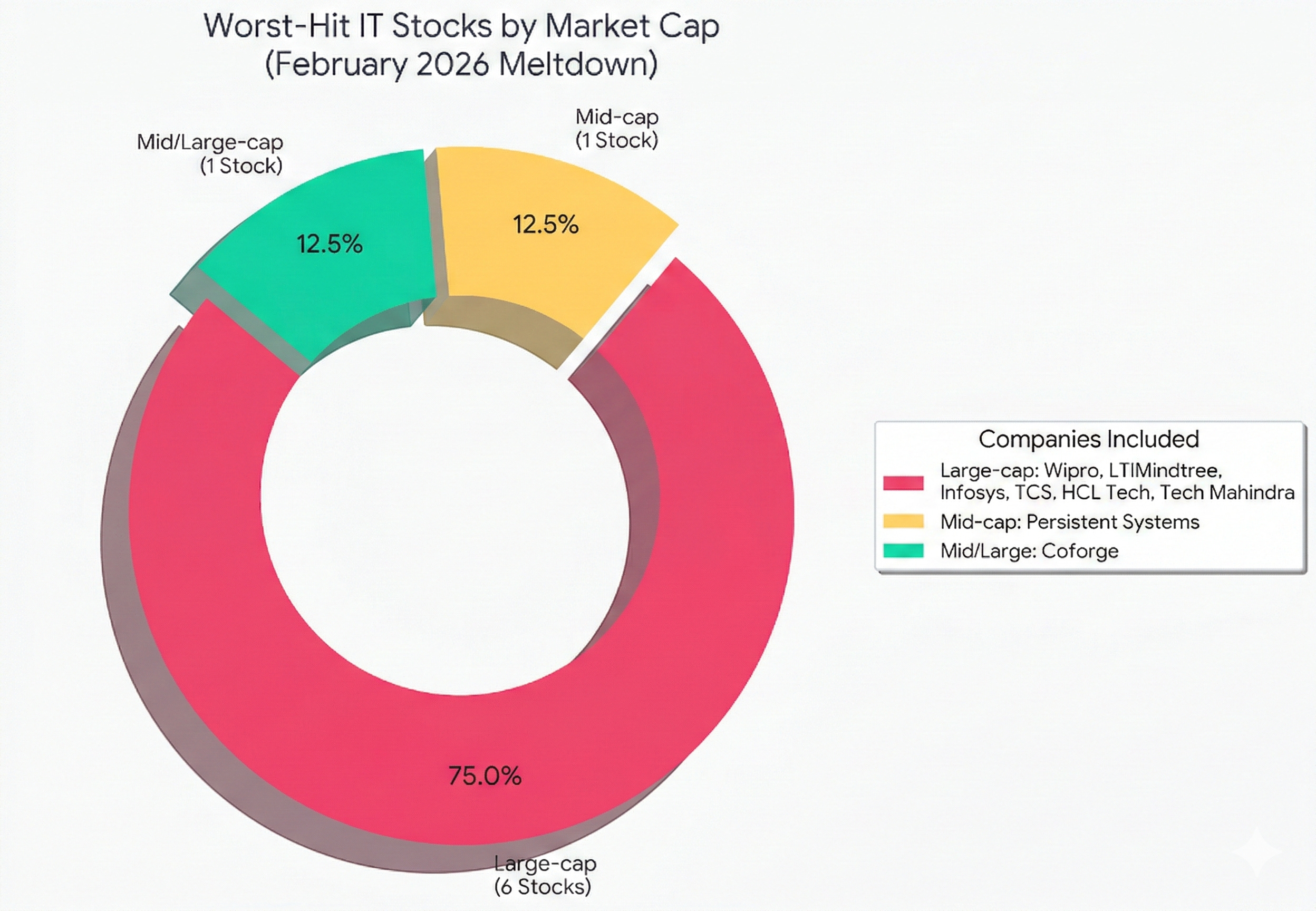

Stocks that fell the most in February 2026

Wipro

Large-cap

Slipped more than 20% in CY26 up to late Feb; part of the worst-hit Nifty IT basket as AI concerns escalated.

Coforge

Mid/large

One of the sharpest losers; down about 4–5% in key sessions, and over 20% for CY26; repeatedly cited as among the top laggards.

LTIMindtree

Large-cap

Included in the group of names that corrected more than 20% year‑to‑date by late February on AI and demand worries.

Persistent Systems

Mid-cap

Prominent casualty; fell more than 4% in single sessions and over 20%+ in the broader February slide.

Infosys

Large-cap

Dropped about 3–4% on multiple heavy‑selling days and was counted among names down 20%+ for the year by late Feb.

TCS

Large-cap

Sold off 3–4% on intense AI‑news days; also cited as down 20%+ YTD within the Nifty IT basket.

HCL Technologies

Large-cap

Fell over 4% on some sessions and over 20% for CY26 as per sector performance summaries.

Tech Mahindra

Large-cap

Included in broker target cuts and in the list of stocks that saw 20%+ correction with the IT index breakdown.

There are fears that these tools could threaten routine tasks in the sector, including software development, debugging and system maintenance jobs, accounting for almost 30% of Indian IT revenues.

Despite these threats, analysts from JP Morgan and Goldman Sachs think that the markets may be overreacting, as AI tools may specialise in a specific task, but the complex task of integrating these tools still requires the expertise and scale available only with the Indian IT giants.

What the market is really pricing

What the market is really pricing is not an “AI apocalypse.” It is a slower, messier earnings conversion cycle. Clients are breaking large transformation programs into smaller pilots, stretching deal-to-revenue timelines and delaying ramp-ups. At the same time, pricing is shifting away from time-and-materials toward outcome-based contracts, which compresses near-term billing and forces vendors to absorb more delivery risk upfront.

The old margin lever, fresher-heavy pyramids, becomes less powerful when AI reduces the need for large teams and raises the premium for specialised talent. Add higher AI-related costs across hiring, training, tooling, and compute, and you get a near-term margin squeeze even if revenue holds up. Finally, the ROI timeline is still unclear, because many AI projects look like experimentation today, not scaled revenue streams tomorrow. That combination is what drives a re-rating: uncertainty moving from “macro demand” to “business model mechanics.

What to watch

These developments should be an eye opener, with the future of the IT sector depending on how the companies offer strategic solutions that matter. Much depends on how the sector uses AI to enhance their skill sets, and how well they are able to implement this in their projects.

For investors, this means tracking:

Deal conversion timelines: are mega-deal wins converting to revenue, or are clients delaying ramp-ups?

Pricing commentary: Are companies disclosing outcome-based contract structures in earnings calls?

Utilisation and fresher hiring: falling utilisation and hiring freezes signal demand weakness before revenue does.

AI revenue disclosure: which companies are breaking out AI-specific revenue, and what is the trajectory?

OPM trajectory: can companies hold margin while investing in AI talent and platforms?

Client budget commentary: what do the large US enterprise clients say about IT spend in their own earnings calls?

February’s selloff is not just ‘AI fear’. It is the market questioning whether India IT can keep the same revenue-to-headcount equation and the same margin structure. If the sector proves it can monetise AI without surrendering pricing power, the premium returns. If it can’t, this is a re-rating, not a dip.

Disclaimer: This newsletter is for informational and educational purposes only and does not constitute investment advice or an offer/solicitation to buy or sell any securities. Views expressed are based on publicly available information as on the date of publication and may change without notice. If any past performance or return figures are mentioned, they are for context only - past performance may or may not be sustained in the future. Please consult a qualified financial adviser before making any investment decision.